Overview:

The costing processes have these variants for different types of costing we decide based on the business processes as which is the better process for the costing purpose.

Joint product costing is a process of costing we need to apply in the cases where there are more than one output gets generated from a production process, where we create the production order for the Main material but the Joint products are also produced as a part of the production cycle and the value of that joint product is also substantial in nature, as that joint product has also consumed the portion of raw materials and other production overheads.

In this scenario we just can’t load the total cost of production of raw materials and production overheads on only one main product.

The joint products also should share the total cost of production in some proportion with the main product.

This will give the proper costing of main products and all the joint products, the cost sharing ratio can vary depending on the types of joint products.

By product costing is a process of costing by which we give the benefit of by product cost or value to the main product. The product generated from the production process will qualify for byproduct only if the market value is minimum or negligible as compared with the main product.

Total cost of production for the main product again will comprises of RM Cost and Production overheads, though the byproducts also consumes some of the raw materials and production overheads during the process of production, but unlike in joint product costing we cannot share the cost with byproduct as these byproducts are negligible in valuation.

Hence as per the globally accepted costing practices we give the credit of the by-product quantity with market value to the main product.

This will ensure the actual costing of the main product after the credit of the by-product and the by-product gets valued with the “net realizable value”

How to achieve these costing solutions in SAP

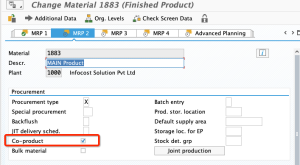

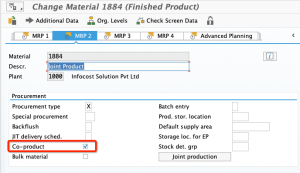

2MM of Joint Product:We need to set the Co Product indicator in the MRP 2 view of Material Master for Joint products.

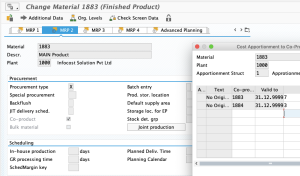

3. Apport.Str of Main Product and same structure we need to maintain in the joint products as well.

For sharing the cost we have maintained the ratio between main and joint products as 7:3

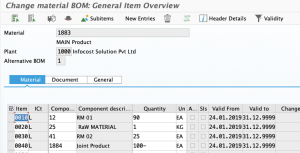

4. BOM of Main Product

Joint product output is 100 quantity with a production lot of 100 main product.

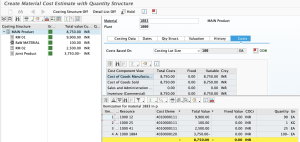

5. Costing of Main Product

Total Cost of Main product production : 12,500*70%=8,750/-

Per unit cost of joint product is : 8750 / 100 = 87.50

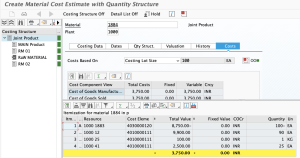

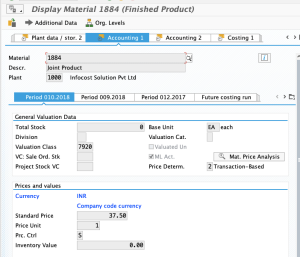

6. Costing of Joint Product

Total Cost of Main product production : 12,500*30%=3,750/-

Per unit cost of joint product is : 3750 / 100 = 37.50

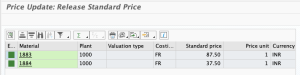

7. Cost Release for both

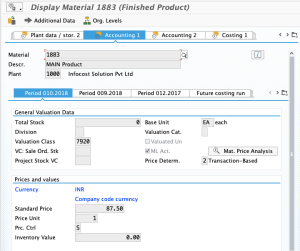

8. MM of Main Product after costing release, it is appearing as the standard price of main product.

9.MM of Joint Product after costing

Conclusion:

Thanks

CA Sarat Agrawal

Professionally Certified SAP CO Consultant

Director @ Infocost Solution Pvt.Ltd. Mumbai, India.

Fell free get in touch with us via phone or send us a message